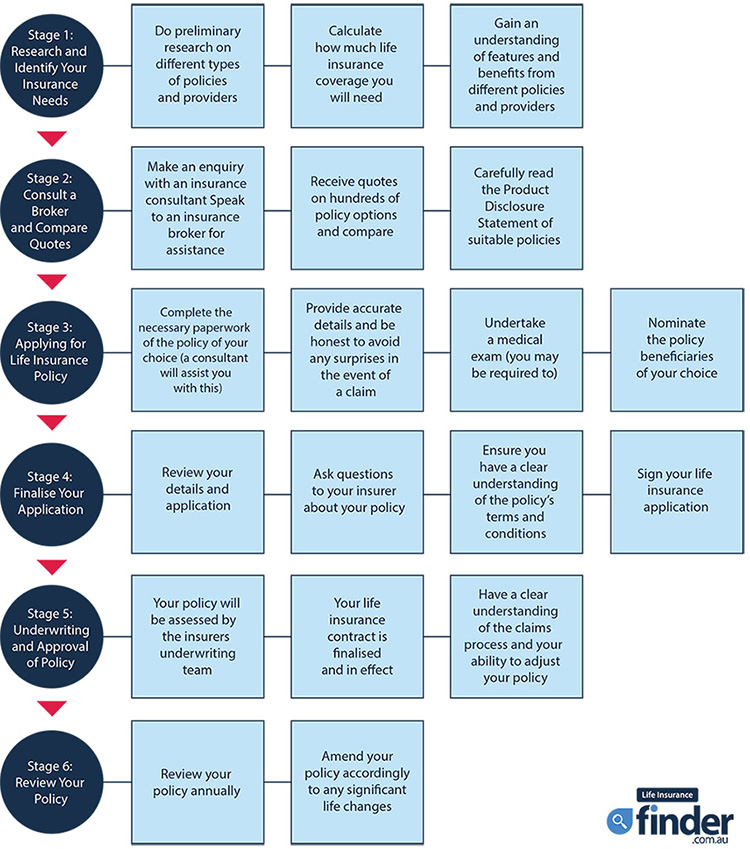

Insurance Services

We take pride in protecting an individual's greatest asset - the ability to earn a living. Whether we are working with person(s), corporation or any other entity type, we offer one of the industry's largest and most comprehensive product portfolio. Our proactive consultative approach to customer service includes working closely with our multitude of product provider's to ensure that we provide the most appropriate products and services for the benefit of the clients. In this way, we strive to protect both the assets, and the financial futures of the clients and their families to the best of our professional abilities. We work with a multitude of insurance companies covering almost every aspect of insurance.

It's never too late to gain control regardless of where you are in the GAME. We will serve as your trusted partner throughout the process. We'll collaborate and work closely to develop and implement a plan so that can enjoy the kind of retirement you've always imagined.

TYPES OF INSURANCE

LIFE INSURANCE

Whole Life

With a Whole Life policy you generally pay a fixed premium over the life of the policy. The younger you are when the policy is purchased the lower the premiums. A portion of each premium covers the cost of insurance and a portion is allocated to a savings component known as the cash value. Income accumulated as a part of the cash value isn't taxed until the policy is surrendered. You can borrow your cash values at a favorable interest rate without triggering taxation of the accumulated earning, or the cash values can be remitted to the insurance company to purchase additional paid-up insurance. Some policies add a portion of the cash value to the death benefit.

Term Insurance

- Term insurance is the least expensive form of life insurance if you believe your life insurance needs will disappear after your dependents have left home or after you have retired. There are three types of term insurance policies available: (1) Annual Renewal Term (ART), (2) Level Term Insurance, and (3) Decreasing Term Insurance.

- Annual renewable term typically provides a level amount of life insurance coverage. It is usually the lease expensive form of life insurance coverage. The cost increases annually. The policy automatically renews each year when the premiums are paid.

- Purchase annual renewable term (ART) insurance that is guaranteed renewable until you are at least age 65. A policy is guaranteed renewable if it can be renewed regardless of your health. ART policy premiums may increase annually.

- Level Term insurance is designed to allow the life insurance coverage and premiums to remain level for a specified period of time, usually 3, 5, 10, 15 or 20 years. Over long periods of time, the cumulative cost of level term insurance is generally less than the cumulative cost of ART. To be sure that the premiums remain level during the period of years, purchase a policy that is fully guaranteed.

- Level term insurance will be more expensive than ART if the coverage is dropped within the first few years.

- Do not purchase a policy that requires re-entry in order to renew the policy term at favorable rates. To re-enter you must pass a physical examination. If you don't pass, the premiums will escalate. Most level term policies can be renewed at a level premium until age 65 at which time rates will increase annually.

- When comparing the cost of various ART and/or level premium term policies having the same benefit, select the policy with the lowest discounted present value premium amount. Ask your financial planner to calculate this figure for you.

- To determine which level term policy will have the lowest renewal premium over the next holding period, ask your agent for the policy's 10-year net payment cost index. The policy with the lowest index may be your better buy.

- Cash value policies are generally less expensive than term policies if the holding period is greater than 15 years. If you are age 50 and you have a continued need for life insurance you should consider converting your existing term insurance into a cash value policy. At about age 50 cash value policies can be less expensive than term insurance over the remainder of your life. One major positive aspect to converting from term to a cash value policy is that most companies will not require you to pass a medical exam to be eligible for the permanent policy.

- Buy enough insurance to meet your needs. If the only way you can presently afford the needed coverage is through term insurance, then buy term. If your financial situation changes and you can afford the higher premiums of level term or permanent cash value insurance, then make the switch. Some term policies may be convertible to cash value policies.

- Decreasing term insurance coverage decreases annually while the premium remains level. It is typically the most expensive form of insurance coverage and should be avoided.

DISABILITY INSURANCE

The probability that you will experience a disability that will last more than 90 days is statistically more likely than the probability of your premature death even at age 60. For this reason, disability insurance coverage is of primary importance in your financial planning. Your personal resources and your disability insurance policy should be able to replace at least 60 to 70 percent of your pre-disability income. Disability insurance provides you monthly payments when you are unable to work because of illness or injury.

Short term disabilities can usually be covered by your emergency fund and savings, vacation or sick leave benefits, or in some cases, short-term disability coverage available from your employer.

HEALTH INSURANCE

You can typically obtain managed health care through your employer, a group such as a chamber of commerce, or as an individual through one of three options: (1) A Health Maintenance Organization (HMO), (2) a Preferred Provider Organization (PPO), or (3) a Point of Service Plan (POS).

a. Health Maintenance Organization (HMO)

An HMO is a defined group of doctors and hospitals. HMO's can offer lower prices than other insurers partly because they sign up doctors and hospitals on contracts that give them volume discounts ranging from 10% to 40% on doctor services and hospital stays. Bigger HMO's can get larger discounts than smaller ones can. To gain access to specialists or hospital services, most plans require you to have the recommendation of a gatekeeper physician. Fees for services range from nothing to $30 and there is no deductible. The doctors may practice in a clinic or hospital, or work in private offices. All types of medical care is covered. The HMO plan usually has the lowest monthly cost.

b. Preferred Providers Organizations (PPO)

A PPO is a network of physicians and hospitals that agree to provide medical care to employers at a discount. You can also get care outside the network. The plan will reimburse you 80% to 100% of the cost of services if you use a doctor or hospital that is part of the network, or 50% to 70% for a service provided outside the network. The plan has a reasonable annual deductible that you must meet before you are reimbursed. The annual deductible is higher for access to physicians or doctors outside the network. Preventive health care services may be covered. Generally you are not required to have the approval of a gatekeeper doctor to gain access to specialists and hospital services.

c. Point of Service Organizations (POS)

A POS is a combination of an HMO and a PPO. The POS is a network of doctors and hospitals, but you can also opt for treatment outside the network. In either case, you must get the approval of a physician gatekeeper in order to access specialists and hospital services. You pay a flat fee from $15 to $35 for care within the network and you also pay an annual deductible. For care outside the network you pay between 20% and 50% of the charges. Preventive care is generally covered.

AUTO INSURANCE

Review your automobile insurance at least annually. When reviewing your coverage, consider the following ideas:

- Liability limits should be at least $100,000 for one injury, $300,000 for all injuries, and $50,000 for property damage. Be sure to carry uninsured motorist coverage unless you live in one of the few states that has no-fault insurance laws. No-fault insurance states generally require your insurer to pay for your damages even if someone else caused the accident. If you do live in a no-fault state you may have to buy personal injury protection (PIP). This covers your medical bills and a portion of lost wages if your are disabled in an accident.

- Premiums can be reduced by raising the deductible limits on comprehensive and collision coverage.

- Before you buy a new car, find out the cost of automobile insurance--it may cause you to want to buy a less expensive car or a different model.

- Take advantage of auto insurance discounts. Discounts are given for the following reasons: (1) A good driving record, (2) the use of anti-theft equipment, (3) senior citizens, (4) successful completion of driver education and training courses, (5) multiple cars insured with the same insurer, (6) a nonsmoker, (7) a nondrinker, (8) participation in car pools, (9) the use of passive restraint devices, (10) college students, (11) low yearly mileage, and (12) students who are drivers and have good grades.

- Do not carry additional insurance coverage, such as towing, car rental insurance, death and disability benefits, or wage loss substitutes. Purchase separate life and disability policies, if needed. Drop towing insurance if you belong to a club like AAA.

- List children who drive as occasional drivers. This will help reduce premium costs.

- Shop and compare auto insurance rates and coverage. It pays off.

- Before you drive faster than the posted speed limit, find out how much a speeding ticket will increase your insurance premiums.

- If you own motorcycles or snowmobiles used seasonally, obtain separate six or nine month insurance policies if it will reduce your insurance cost.

- If you lease your car, the insurer may only pay replacement cost if the car is stolen or totaled. Replacement cost may be thousands of dollars less than the unpaid lease amount. Consider paying a one-time premium to fill this gap.

HOME OWNERS INSURANCE

- Structural coverage should be equal to or greater than 80 percent of the value of your home.

- Review your homeowners coverage at least annually to be sure that it is adequate and that the coverage has been adjusted for appreciation.

- Coverage on furniture, personal possessions, collectibles, jewelry, etc. should be equal to their replacement cost.

- Purchase replacement cost coverage rather than actual cash value coverage. Obtain replacement cost coverage on the home, furniture, and personal possessions.

- Inventory all household articles by item, description, purchase date, cost, and appraised value, if any. Consider making a video recording or taking photographs of household articles and keeping them with the inventory. The inventory and the video recording or photographs should be kept off-site in a safe deposit box or in some other safe location.

- Purchase a personal articles floater to insure expensive personal items, such as collections and jewelry.

- If you own a personal computer find out whether the policy covers damage to software and hardware caused by a power surge or software virus, and theft or damage to laptops and notebooks outside your home. If the policy doesn't provide coverage you may be able to buy a rider that does.

- Ask your agent to explain the details of your coverage and whether all covered items have to be included in your policy.

- Do not purchase earthquake and flood insurance unless you are in a government- designated earthquake zone or flood plain.

- If you are renting, purchase a tenant's policy.

- If you own rental property, consider purchasing an owners, tenants and landlords policy.

- Your premiums can be reduced by raising the deductible to $500 or more.

- Consider liability coverage of at least $300,000.

- If you own a condominium consider obtaining coverage to help cover your responsibility as a unit owner to pay some of the homeowner association deductible or uninsured loss incurred by the association and assessed to you as a unit owner. The loss must be a result of a peril covered under the unit owner policy. Carefully compare your personal insurance contract with those of the association to identify possible gaps in coverage.

UMBRELLA LIABILITY INSURANCE

Umbrella Liability Insurance provides additional coverage when your personal liability coverage under an automobile and homeowners policy ends. Adequate liability coverage will protect you from a legal judgment against your future income. When purchasing Umbrella Liability Insurance, consider the following:

- Purchase an amount at least equal to your net worth, and any additional legal costs for your defense. Typically, umbrella liability insurance is purchased in one million dollar increments.

- Coverage is usually coordinated with auto and homeowners coverage. Therefore, it may only be available to you through your primary property and casualty insurer. The annual premium for a one million-dollar policy should be less than $200.

- If the policy stipulates that the cost of your legal defense will be subtracted from the face value of the policy, consider increasing your coverage.

- Be sure that the policy has provisions for the coverage of children who are away at college and a provision for the payment of claims that arise from damages caused by your pets and animals.

- Find out whether the policy requires disclosure of potential liabilities to the insurer.

LONG TERM CARE

Long-term Health Care Insurance provides coverage for a long-term illness that results in a nursing home stay or in-home nursing care. The average cost for a one-year stay in a nursing home is approximately $150,000 to $400,000 depending where you live in the United States. If you are approaching retirement or you are currently retired, consider offsetting the costs of an extended nursing home stay by purchasing long-term health care insurance. Long-term health care insurance is ideal if: (1) you have assets in the $200,000 to $1,000,000 range, (2) you want to preserve those assets for your children, and (3) you can free up about 2-5% of your annual income to cover the premiums. Long-term health care insurance comes in two broad varieties: "Qualified" coverage, the cost of which may qualify as a medical deduction on schedule A of your tax return, and "non-qualified" coverage. Premiums you pay for qualified long-term care insurance are deductible as a medical expense subject to certain limitations. A qualified long-term care policy must meet the provisions of Internal Revenue Code section 7702B.

Medical Services That Should Be Covered

- Skilled, intermediate, and custodial levels of care. Covered custodial care should be available in senior day-care centers and assisted-living facilities also known as congregated care centers.

- Home care coverage. Look for a policy provision that specifically covers home health care that meets state licensing requirements, if any. The daily benefit should be at least 75% of the benefit payable for nursing home care.

- Optional respite care. Option respite care is a short nursing home stay to allow families providing home care a short break.

- Alzheimer's Disease and Senility. Avoid contracts that only cover demonstrable organic illness. Alzheimer's Disease can only be definitively proven with a brain biopsy. Benefits should be payable based on a doctor's diagnosis.

- A preexisting condition exclusion of six months or less. This clause will ensure that you will be covered for conditions that take longer than six months to show up such as Alzheimer's.

- Multiple stays in the hospital

- Costs of care rendered after you return home to convalesce

- Optional adult day care

We follow the fiduciary standards by making sure all of our recommendations are based on your specific needs and are truly suitable for you personally. Your needs always come first, before our compensation.